For Poly, you really need to get closer to sell out before you can definitely determine reliable patterns as to how often and how fast bungalows can fill. For example, last year Poly was new, Disney was entitled to most use of the bungalows based on points sold and thus owners had minimal time they could reserve, you always have a large group of owners from other resorts at the beginning that wants to try something once, and persons from other resorts were actually in a better position to reserve them at the high point cost because they did not have to pay $165 a point to get their points. Also, seeing them filled for the high demand late Sep 2016 to early Jan 2017 period at this point does not provide a true picture because Disney could stick a small tent on the beach, charge 100 points a night, and fill it by four months out for that time of year.

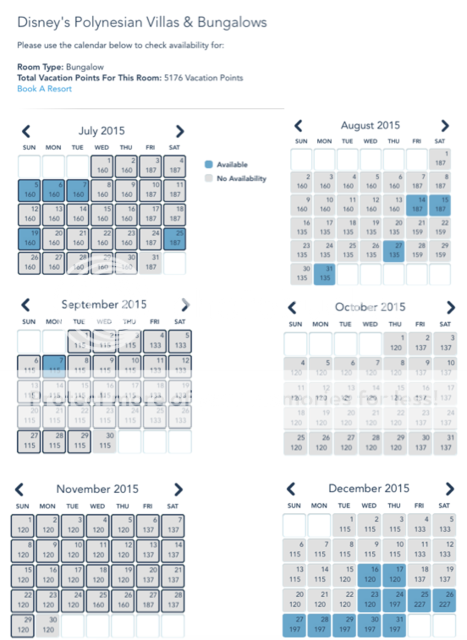

The bungalows have been a mixed bag for 2016 but it is still too early to tell what the real pattern will be. For example, mid-Jan through March was open at both 60 days and 30 days out except for Presidents weekend, Princess half marathon weekend and two days in mid-March, but DVD added 6 bungalows to DVC inventory in Jan and possibly rooms were open partly because the new rooms had just been added. Just before February 24, April was showing 12 nights filled (10 of those during Easter week and the week after); May had five nights filled, two in early May and three during Memorial Day weekend; early June had two filled; and July 3 and 4 were gone with the rest of the year open. Then a strange thing happened on February 24. The last week of April through June 9 filled at the same time. I do not know the explanation but question whether all those rooms and dates were actually reserved at the same time. Some of those dates in May and June days opened up later, and at the end of April, June still had 20 days open.

In early June another strange event happened resulting in 21 days of July and 27 days in Aug showing as filled. However, that changed and on June 20, July was open for 27 days, and Aug was open for 21 days. On July 8, July still had 10 days in the remainder of the month still open while Aug was still open for 12. At the end of July, September had 12 days open. October through Dec filled on average about 4 to 5 months out although a small number of dates in mid-Oct, race weekend in November, Thanksgiving time, first week of Dec and Christmas week filled near the 7-month window.

The fill rate for bungalows has been slower this year than for the VGF GV's but, of course, there are only 6 GV's. Those GV's also had many days open at 60 days out during the mid-Jan to late Sep time period but not near as many as Poly. Currently the bungalows are open mid-Jan 2017 and thereafter, matching SSR GV's, but other GV's are showing more fill time.

I do not perceive any reason to lower Poly bungalow points and raise studios. That should never be done just because bungalows are not filling before the breakage point at 60 days out. That would also be true for any resort that has GVs. The only possible reason to ever lower bungalow and raise studio points would be because the studios are showing serious reservation problems, but Poly is not showing that. Poly studios have had no issues of filling quickly at the 11-month window -- for the mid-Jan to late Sep period this year (and thus far next year through late March), they were usually open at 7 months out and beyond. For the late Sep to marathon weekend in Jan period, only some of the very high demand dates filled before 7 months out this year. Open dates did tend to fill extremely quickly at 8 a.m. at 7 months out, but as a near park resort, Poly stood alone in even having studios to get much of the time at 7 months out. Moreover, that high demand quarter is a seasonal issue for all of WDW DVC and thus the fix, if any, would be shifting points among seasons not between the bungalows and studios. Poly's situation is likely to become somewhat worse as it approaches sell out, but with the huge number of studios it has, it has a decent chance of avoiding problems like the one that has developed at VGF where studios can be difficult to get even at 11 months out at a number of times during that high demand last quarter of the year.

The issue I perceive with Poly is the future of DVC that it is creating, which actually started with VGF. In the 2 1/2 year period before VGF went on sale, Disney raised the price per point for BLT, after it was already close to sell out, by 40% when inflation was next to nothing. Thus, when it introduced VGF at a price just below BLT, Disney was able to create the impression among purchasers that VGF was a bargain when, in fact, it was being sold at a price much higher than almost all of BLT had been sold. Added to the increase in price was an increase in points needed per night at VGF for like rooms over BLT, thus adding to the increased cost to the purchaser. That high price per point and points per night, along with a low 100 point minimum purchase for new purchasers, and the low number of studios at VGF, caused the problem that exists now at VGF for getting studios because far too many purchased there to get only studios.

That oversell-of-studios business model continued with Poly, but sheer numbers of studios might save it from having the VGF 11-month problem. There is still only a 100 point minimum. There is the very high price per point combined with high points per night. Then there are the bungalows which add a huge number of points to sell to mostly purchasers who are buying enough points to get only studios, e.g., it is not likely you are going to have large numbers of purchasers spending the $200,000 needed to get a week during magic season in a bungalow. That kind of purchaser has never been Disney's target audience. Moreover, there is no in-between option for purchasers to decide to purchase enough points to possibly get a 1BR or 2BR; thus the decision being made by most purchasers is to buy only enough points for a studio even if they could afford more. Disney is creating a huge class of owners who have enough points to get only studios, including when they look to reserve other near park options at 7 months out. Meanwhile, Disney has created the five person studio at other near park DVC resorts that exists with Poly. Thus, one of the effects of the Poly model will be to significantly increase the demand for studios at the 7-month window for other near park resorts.

In addition, Disney gets the best of all worlds with the bungalows. It has created signature accommodations that it can put on advertisements promoting WDW in general and passes on the costs of building them to DVC purchasers. It can charge large amounts a night for a number of them when not reserved by 60 days out by members, and likely that is going to end up being for a significant amount of time. And that breakage rental income will be almost all profit. except for a small percentage that goes to offset dues, because it is those Poly DVC members who purchased to get only studios who are going to pay for the operation and maintenance of those bungalows through dues. That model seems to be carrying over to the new Copper Creek at WL with the creation of cabins on the beach that are likely to also cost a fortune in combined price per point and points per night, although Copper Creek may end up having something other than studios in the redone portion of WL. In other words, with Poly and soon-to-be Copper Creek, Disney has discovered the way to increase its hotel business, at least part-time, with signature units, and have someone else, the DVC members, pay for the construction and maintenance of those units.

A random point for which the explanation may arguably be that Disney does not really want members taking the bungalows once you are at the 60-day window is that the new tool on its site that tells what is still open at 60 days out usually has not provided most of the bungalow days that are still open. Of course, the explanation could alternatively be the usual one, that Disney's IT group has once again created a system that does not work correctly.